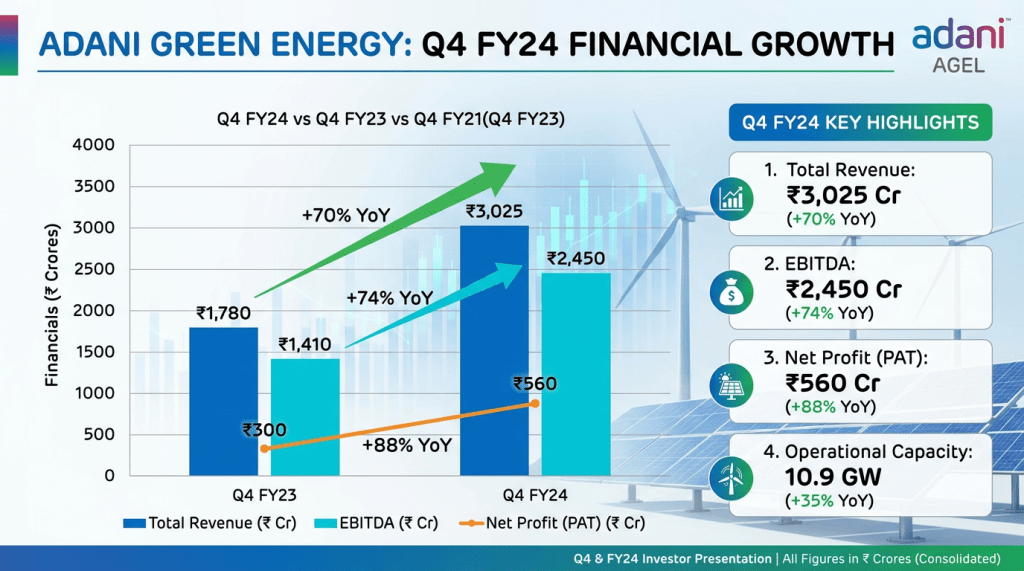

Adani Green Energy’s board cleared its audited results for Q4 FY26 and FY26 with a clean audit opinion. While the exchange filing focused on approvals and board decisions rather than line-by-line numbers, the big picture is steady governance signals. The detailed PDFs on the exchanges and the company website will carry the full financials; until then, here’s what matters and why it matters for investors.

Quick Summary: Adani Green Energy Results

- Audited results for Q4 FY26 and FY26 approved; auditors gave an unmodified (clean) opinion.

- Re-appointment of three Independent Directors effective Sep 2026, signalling continuity.

- Joint Statutory Auditors appointed/re-appointed; new Internal Auditor named for tighter controls.

- Leadership tweak: new Head – Business Development & Strategy; AGM on June 25, 2026.

Adani Green Energy Financial Highlights

- Period covered: Q4 FY26 and full year FY26 (Standalone and Consolidated – audited).

- Audit opinion: Unmodified on both Standalone and Consolidated financials by joint statutory auditors.

- Statements filed: Profit & Loss, Balance Sheet, and Cash Flow Statement (for the half year ended March 31, 2026) along with auditor’s reports.

- Where to find numbers: Company website (www.adanigreenenergy.com) and stock exchanges (BSE 541450, NSE ADANIGREEN).

- What to scan first when you open the PDFs:

- Revenue growth YoY/QoQ ↑/↓

- EBITDA and EBITDA margin

- PAT/Net Profit and any one-time items

- Operating Cash Flow vs EBITDA (cash conversion)

- Net Debt, cost of debt, and interest coverage

- Capacity added (MW) and plant load factors/CUF by solar, wind, and hybrid

Why Key Numbers Changed (Important Insight)

- Revenue vs Profit – why they move differently:

- Revenue can rise with new capacity commissioned and stronger resource (sun/wind) ↑, but profit may lag if interest, depreciation, and start-up costs jump at the same time.

- In renewables, large projects add big fixed costs upfront (depreciation, interest). So profit often trails revenue growth in early years.

- One-time items to watch:

- Forex gains/losses on foreign debt or equipment imports can swing profit ↑/↓.

- Fair-value changes on derivatives, impairment/asset write-backs, or reversal of provisions can temporarily inflate or depress PAT.

- Margin changes (EBITDA and PAT):

- Mix shift matters: more wind in high-wind months can lift CUF and margins ↑; lower irradiation or curtailment can pull them down ↓.

- O&M efficiency, inverter/replacement cycles, and grid availability directly affect EBITDA.

- Financing cost trends (refinancing at higher/lower rates) flow through to PAT margins.

- Cash flow vs accounting profit:

- EBITDA can look healthy while operating cash flow lags if receivables from DISCOMs stretch.

- Conversely, steady collections can show strong cash flow even in a soft resource quarter.

Operational Performance & Business Trends

- Capacity and mix:

- Growth typically comes from new solar, wind, and hybrid projects entering commercial operation.

- Hybrids help smooth seasonality and can support better utilization and grid compliance.

- PPAs and counterparty quality:

- Central agency PPAs (e.g., SECI) tend to mean steadier payments; state DISCOM exposure can add receivable risk.

- Execution and pipeline:

- The appointment of a Head – Business Development & Strategy signals focus on building and converting the project pipeline.

- Cost curve and supply chain:

- Module and turbine cost trends, logistics, and forex rates impact project IRRs and margins.

Management Commentary (Simplified)

- Clean audit opinion: Management is signaling confidence in reported numbers and controls.

- Re-appointment of Independent Directors: Continuity on the board, steady oversight.

- Auditor moves: Keeping joint statutory auditors and adding a new internal auditor point to stronger checks and processes.

- Leadership change in Business Development & Strategy: Emphasis on growth pipeline and disciplined project selection.

Key Positives

- Unmodified audit opinion – a credibility boost with investors.

- Stronger assurance framework with joint statutory auditors and a new internal auditor.

- Continuity via re-appointment of three Independent Directors from Sep 2026.

- Dedicated focus on pipeline with a new Head – Business Development & Strategy.

- AGM date fixed (June 25, 2026), indicating timely disclosures and engagement.

Key Concerns

- Full financial details weren’t in the summary text; investors should review the PDFs for numbers and notes.

- Sector risks: DISCOM payment delays and grid curtailment can squeeze cash flows.

- Leverage and refinancing needs are inherent in utility-scale renewables; interest-rate swings matter.

- Resource variability (irradiation/wind) can cause quarterly volatility in CUF and margins.

- Regulatory/tariff changes or commissioning delays can affect returns.

Final Takeaway for Investors

Clean audit and governance continuity are clear positives. The investment call now rests on the actual FY26 numbers: revenue growth versus capacity additions, EBITDA margin resilience, cash collections from customers, and the trajectory of net debt and cost of debt. Review the detailed filings before deciding. If the company shows strong cash conversion and disciplined leverage alongside capacity ramp-up, the long-term story holds. If receivables, interest costs, or one-offs pressure PAT and cash flow, expect near-term volatility.

FAQs

- What is revenue?

- Money earned from selling electricity under PPAs and any related operating income.

- What is profit?

- What remains after all expenses: operating costs, depreciation, interest, taxes, and any one-time items. Net Profit (PAT) is the bottom line.

- Why did profit change?

- Even if revenue rose ↑, higher interest and depreciation from new plants, forex swings, or one-time gains/losses can move profit up or down.

- What should I check first in the results?

- EBITDA margin, operating cash flow vs EBITDA, receivable days, net debt and cost of debt, and capacity/CUF trends.

- Is it a good stock?

- Depends on your risk appetite. If you can handle sector/regulatory swings and leverage-driven models, review the latest numbers and outlook. If you want smoother cash flows and lower debt, wait for clarity on collections and refinancing.

Disclaimer

This post is for educational purposes only. It is not investment advice. Please read the company’s official filings and consult a financial advisor before making investment decisions.