Quick Summary: Adani Energy Results

- Transmission network availability held near best-in-class at 99.70% ↑

- Mumbai distribution losses improved to a low 4.21% in FY26, supporting margins ↑

- Raised Rs 8,373 crore via QIP to strengthen the balance sheet; international ratings at BBB- / Baa3 maintained ↑

- Growth pipeline intact: presence across 14 states in transmission, smart metering in 5 states, and renewable evacuation (HVDC/Khavda) progress ↑

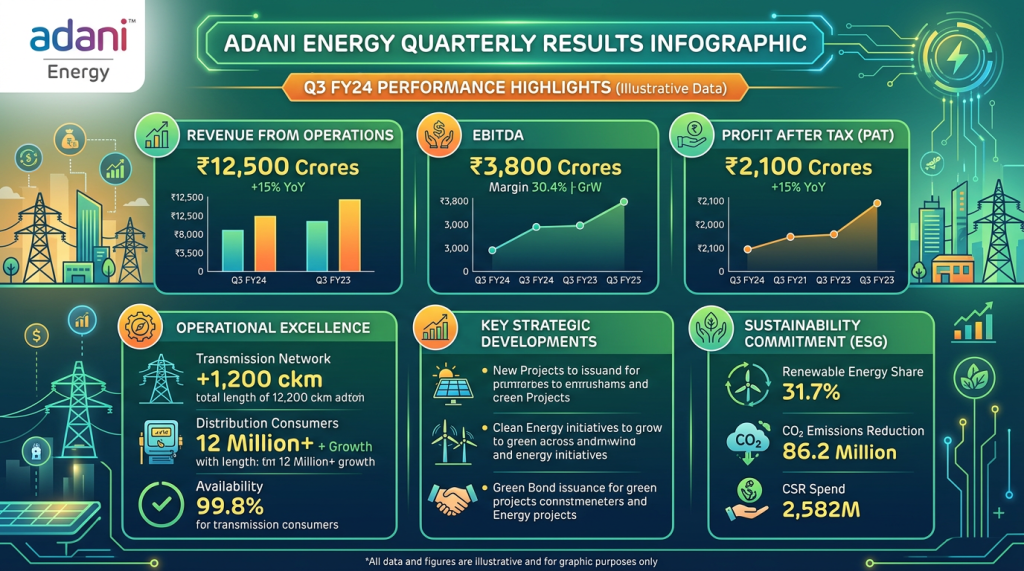

Adani Energy Financial Highlights

- Status: Q4FY26 update is provisional and operational; audited revenue, EBITDA, and PAT were not disclosed in this note.

- Transmission

- Network length: 27,949 ckm

- Availability: ~99.70% (supports full tariff recovery)

- Sector-leading transmission EBITDA profile (company cites ~92% margin for the segment)

- Distribution (AEML – Mumbai; MUL – Mundra)

- Consumers served: 13 million+

- Distribution loss (AEML, FY26): 4.21%

- RAB in Mumbai Discom: ~8% CAGR since acquisition

- Smart Metering and Renewables

- Smart meters: presence in 5 states; potential base of ~99 million consumers

- Auxiliary solar installed: 3.36 MWp at substations

- Capital & Liquidity

- Equity raised: Rs 8,373 crore via QIP

- Investment-grade ratings: BBB- / Baa3, access to long-tenor, low-cost capital

Why Key Numbers Changed (Important Insight)

- Availability drives revenue: Transmission revenue in a regulated model depends on asset availability. Sustained ~99.70% availability enables near-full tariff recovery, stabilizing top line and cash flows.

- Lower losses lift margins: AEML’s loss level at 4.21% reduces power purchase leakage, which typically supports distribution EBITDA and cushions profit even if demand is uneven.

- Balance-sheet repair now, earnings later: The Rs 8,373 crore QIP reduces reliance on debt. Interest cost benefits show up gradually; near term, earnings can still reflect depreciation/interest from projects under execution (HVDC, renewable evacuation lines).

- Regulatory true-ups matter: Utilities often recognize tariff true-ups, carrying cost, and FX adjustments in batches. These non-linear items can swing quarterly profit without reflecting a fundamental change in operations.

- Mix shift to regulated assets: As the portfolio tilts further to regulated transmission/RAB-based distribution, earnings volatility decreases, but reported profit is more sensitive to regulatory timelines and capex commissioning schedules.

Operational Performance & Business Trends

- Transmission

- Wide presence across 14 states with a network of 27,949 ckm

- Focus assets: longest private HVDC line; continued renewable evacuation buildout (e.g., Khavda)

- Consistent availability near 99.70% underscores execution and O&M strength

- Distribution

- Mumbai (AEML): reliability plus green power options; loss reduced to 4.21% in FY26

- Mundra (MUL): AEML’s consumer-centric and efficiency playbook being replicated

- RAB growth in Mumbai (~8% CAGR) underpins predictable returns

- Smart Metering and Digital

- Deployed across 5 states with a pathway to a potential ~99 million consumer base

- Long-term, metering can unlock better cash collection, lower AT&C losses, and analytics-led operations

- ESG and Decarbonisation

- Solarization of substations (3.36 MWp) and support for green power integration

- Grid strengthening to accommodate rising renewable share

Management Commentary (Simplified)

- We’re doubling down on regulated assets: steady RAB growth and high availability should keep cash flows predictable.

- Capital is secured: the QIP and IG ratings provide room to fund long-tenor projects at competitive rates.

- Customer first: reliability in Mumbai and a push into smart meters will enhance consumer experience and operating efficiency.

- Energy transition is a tailwind: HVDC and renewable evacuation corridors are core to our medium-term growth.

Key Positives

- High transmission availability (~99.70%) and low AEML loss (4.21%) support stable margins ↑

- Large, visible capex pipeline in regulated transmission and smart metering

- Strengthened balance sheet after Rs 8,373 crore QIP; IG ratings maintained

- Wide national footprint across 14 states; proven execution on complex assets like HVDC

Key Concerns

- Regulatory timelines/true-ups can create quarterly profit volatility ↓

- High capex intensity keeps depreciation and interest elevated during build-out ↓

- Distribution profitability remains sensitive to power procurement costs and demand mix ↓

- Group-level scrutiny and market sentiment can impact valuation multiples ↓

Final Takeaway for Investors

AESL’s Q4FY26 provisional update points to a steady operational quarter with strong availability, improving efficiency in Mumbai, and ample growth capital post-QIP. While audited revenue and profit are awaited, the mix of regulated transmission, RAB-led distribution, and smart metering provides long-term visibility. For investors, this is more of a compounding utility story than a cyclical bet. Watch the final results for tariff true-ups, leverage metrics, and commissioning timelines that can move near-term earnings, but the medium-term path remains constructive.

FAQs

- What is revenue?

- Revenue is the total money a company earns from its operations—here, mainly regulated tariffs from transmission lines and electricity distribution.

- What is profit?

- Profit is what remains after subtracting operating costs, interest, depreciation, taxes, and any one-off items from revenue.

- Why did profit change this quarter?

- The provisional note doesn’t disclose profit. Generally, in utilities, profit moves with interest and depreciation from new assets, distribution loss levels, tariff true-ups, and foreign exchange impacts. Lower losses and high availability help, while ongoing capex can keep interest/depreciation elevated.

- What is RAB and why does it matter?

- RAB (Regulatory Asset Base) is the asset value on which regulators allow a return. As RAB grows (e.g., Mumbai at ~8% CAGR), earnings visibility improves because returns are formula-driven.

- Is it a good stock to buy?

- It suits investors seeking steady, regulated cash flows with a long runway in transmission and metering. Risks include regulatory timing, capex execution, and power procurement volatility. Do your own research or consult a financial advisor.

Disclaimer

This post is for educational purposes only and is based on the company’s provisional operational update. It is not investment advice. Always do your own research or consult a licensed advisor before investing.