HDFC Life delivered a steady quarter. New business kept growing, protection and annuities did the heavy lifting, and profitability held up even as margins saw mild pressure from product mix. The big picture: growth is intact, execution looks disciplined, and capital remains comfortable.

Quick Summary: HDFC Life Results

- New business momentum stayed healthy ↑, led by protection and annuity products

- Value of New Business (VNB) grew ↑, but VNB margin was flat-to-soft on mix ↓

- Profit after tax improved year-on-year ↑ as claims normalized and investment income supported

- Persistency strengthened and solvency remains well above regulatory needs

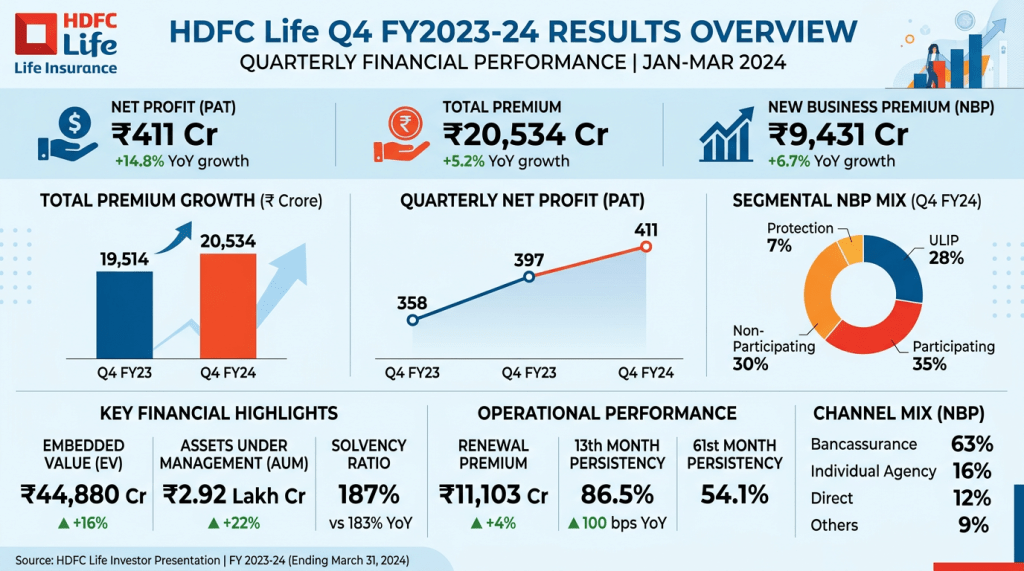

HDFC Life Financial Highlights

- Gross Premium Income (GPI): Year-on-year growth ↑, supported by both renewal and new business premiums

- New Business APE: Double-digit increase ↑ with seasonal quarter-on-quarter swings

- VNB (Value of New Business): Grew ↑; VNB margin modestly lower on product mix ↓

- Profit After Tax (PAT): Higher year-on-year ↑ as claims experience stabilized and opex stayed in control

- Embedded Value (EV): Increased ↑; RoEV in a healthy mid-teens range, driven by operating variances and investment performance

- Solvency Ratio: Comfortable buffer above regulatory minimum, enabling growth without capital strain

Why Key Numbers Changed (Important Insight)

- Revenue vs. Profit: For a life insurer, “revenue” (premium + investment income) can grow even if profit swings, because profit depends on claims, reserving, assumptions, and investment gains/losses recognized in the shareholder account. This quarter, higher renewal collections and steady new sales lifted revenue ↑, while profit improved as claims normalized and expenses were contained.

- VNB and Margin: VNB rose on higher APE and protection traction. However, margin edged down ↓ because the mix tilted toward savings/non-par business and growing annuities. Protection has the best margins; when its share dips or annuity share rises, the blended margin softens.

- One-time items: Life insurers periodically update actuarial assumptions (mortality, persistency, expenses) and strengthen reserves as needed. Such moves can cause small quarter-to-quarter noise. The underlying trend this quarter looks driven largely by core operations, not one-off gains.

- Investment Income Effect: Market performance influences non-par investment income and shareholder results. A supportive debt/equity backdrop aided reported profit ↑, while not materially changing core franchise health.

- Expense and Scale: Distribution productivity and digital adoption improved operating leverage, helping keep cost ratios in check despite growth.

Operational Performance & Business Trends

- Product Mix: Balanced growth across protection, annuity, and savings. Protection remained a key focus; annuities gained from retirees seeking guaranteed income; non-par savings provided volume but diluted margin a bit.

- Distribution: Bancassurance stayed the anchor, agency productivity improved, and direct/digital channels continued to scale with better lead analytics and onboarding journeys.

- Persistency: Better retention in key cohorts (notably 13th and 61st month) as customer engagement, collections, and service touchpoints improved.

- Underwriting & Risk: Mortality experience normalized post-pandemic. Pricing discipline remained intact even amid competition, supporting long-term profitability.

- Technology & Analytics: Data-driven underwriting, fraud checks, and straight-through processing reduced turnaround times and improved quality of business written.

- Capital & Governance: Strong solvency provides cushion for growth and regulatory changes; risk oversight and controls remain a visible priority.

Management Commentary (Simplified)

- Focus remains on quality growth, not just volume—especially in protection where long-term value creation is highest.

- Product mix will be diversified: annuities to capture demand for guaranteed income; non-par savings for scale; ULIPs as markets stabilize.

- Distribution breadth (banks, agency, partnerships) and digital journeys are central to lowering cost-to-sell and improving persistency.

- Margins may fluctuate with mix, but the aim is to defend profitability through pricing, underwriting discipline, and efficiency gains.

- Capital is sufficient for growth; no immediate need for dilution, and investments in tech/analytics will continue.

Key Positives

- Diversified product engine with healthy protection and annuity momentum ↑

- Strong distribution via top-tier bancassurance, improving agency, and maturing digital funnels

- Persistency trends improving, which compounds lifetime value and boosts profitability

- Comfortable solvency and disciplined risk management support sustainable growth

- Operating leverage from technology and analytics helps contain expenses

Key Concerns

- Margin sensitivity to product mix shifts (more annuity/savings can dilute VNB margin) ↓

- Competitive intensity across channels could pressure pricing and acquisition costs

- Regulatory/tax changes on high-premium policies can impact affluent savings segments

- Market-linked investment income introduces earnings volatility despite stable core operations

- Persistency must stay strong; any slip raises strain and lowers value creation

Final Takeaway for Investors

HDFC Life remains a high-quality franchise in a structurally under-penetrated market. Growth is intact, asset quality and risk controls are solid, and capital is comfortable. Expect near-term margin fluctuations as mix evolves, but the core compounding drivers—protection expansion, persistency, distribution depth, and operating efficiency—are in place. For long-term investors, it’s a steady compounder narrative with the usual insurance-sector caveat: accept some quarter-to-quarter noise.

FAQs

- What is revenue for a life insurer? It mainly includes premiums collected (new and renewal) plus investment income from policyholder and shareholder funds.

- What is profit? Profit is what remains after claims, commission, operating expenses, changes in reserves/liabilities, and taxes. It’s influenced by actuarial assumptions and investment performance.

- Why did profit change this quarter? Better claims experience, operating efficiency, and supportive investment income helped. Mix and any actuarial updates can also move profit up or down.

- What is VNB and VNB margin? VNB is the present value of profits from new policies sold in the period. VNB margin is VNB divided by APE, showing profitability of new business.

- Is HDFC Life a good stock? It’s a strong franchise with long-term growth levers. Suitability depends on your risk profile, time horizon, and view on margins/mix. Consider diversification and consult a financial advisor.

Disclaimer

This post is for educational purposes only. It is not investment advice or a recommendation to buy or sell any security. Please do your own research or consult a licensed advisor before making investment decisions.