Quick Summary: Just Dial Results

- Q4 FY26 unique visitors at 182.4 million (↓ vs 184.5 million in Q3) – slight softness in traffic.

- 631,530 active paid campaigns – monetization base intact.

- Platform remains mobile-first: 85.7% of traffic from mobile apps/website ↑ scalability.

- Rich content moat: 54.7 million listings and 157.1 million ratings/reviews support trust and conversions.

Just Dial Financial Highlights

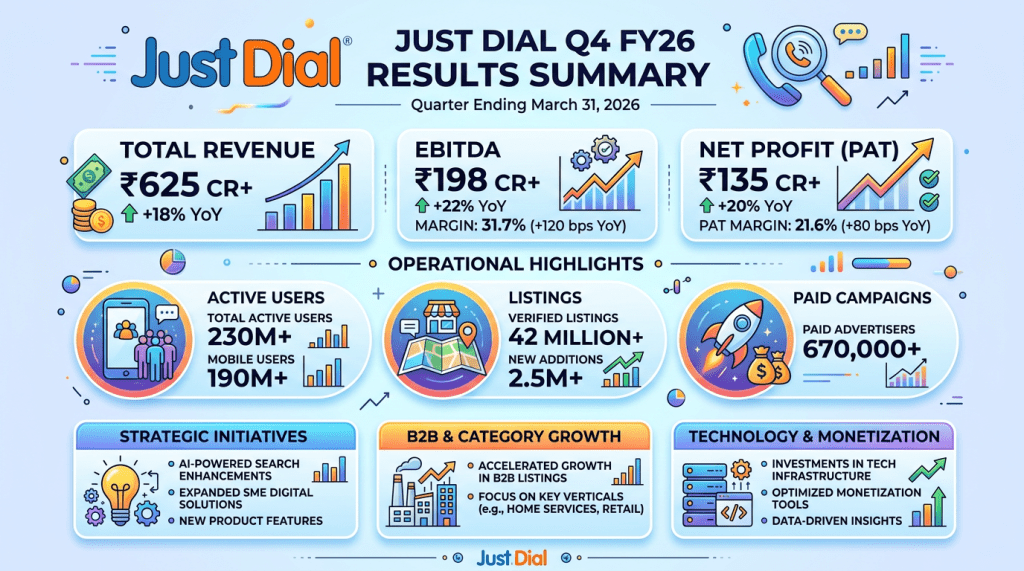

Note: The corporate presentation shared operating metrics but did not include revenue, EBITDA or PAT figures. Below are the key drivers that typically shape financials.

- Business model: Prepaid, subscription-led advertising for SMEs; premium and non-premium listing packages; add-ons like banners, website builder, JD Pay, and ratings tools.

- Monetization base (Q4 FY26): 631,530 active paid campaigns; national and multi-city campaigns for larger advertisers.

- Traffic & reach (Q4 FY26): 182.4 million unique visitors (Q/Q ↓ from 184.5 million); mobile share 85.7%, desktop 11.5%, voice 2.8%.

- Content depth: 54.7 million listings; 157.1 million ratings & reviews enhance credibility and conversion.

- Distribution: On-ground presence in 250+ cities across 11,000+ pin codes; sales engine of 5,122 telesales and 5,350 feet-on-street reps.

- Working capital: Prepaid model typically supports cash flows and reduces credit risk vs. pay-later ad models.

Why Key Numbers Changed (Important Insight)

- Traffic softness Q/Q: The slight decline to 182.4m likely reflects normal seasonality, algorithmic shifts, or tougher comparisons. For a directory-style business, even small traffic moves can affect lead volumes and campaign renewals.

- Revenue vs. profit: Revenue is driven by the number of active paid campaigns and average revenue per campaign (package mix, city tiers, add-ons). Profit moves differently because it absorbs fixed and variable costs (sales hiring, marketing, tech, customer support), so margins can expand or compress even if revenue is flat.

- Margins: A mobile-heavy mix and telesales leverage usually support margins. However, increased spending on sales feet-on-street, brand marketing, or new product builds (JD Mart, JD Omni, JD Xperts) can lower near-term margins to seed future growth.

- One-time items: Not specified in the deck. Typically, items like provisions/write-offs, legal/settlement costs, ESOP charges, or tax adjustments can swing reported profit in a given quarter without reflecting core operating momentum.

- Churn and ARPC dynamics: Upgrades to premium placements and cross-selling add-ons can lift ARPC; SME budget cuts or higher churn can offset that. The active paid campaign count and renewal rates are key indicators to watch.

Operational Performance & Business Trends

- Mobile-first discovery: With 85.7% of traffic from mobile, the company benefits from lower friction and better engagement via app notifications, location detection, voice search, and maps.

- Trust and conversion: 157.1m verified ratings and reviews, photos, and performance tags help users pick the right vendor, improving lead quality for SMEs.

- SME digitization stack: Beyond search, tools like website builder, JD Pay, JD Ratings, JD Omni (cloud solution), and JD Xperts deepens wallet share and stickiness.

- B2B push: JD Mart targets wholesale buyers and suppliers, expanding from local discovery to transactions and quotes – a potential ARPC and category depth driver if scaled well.

- Distribution muscle: Presence in 250+ cities and a large salesforce support penetration into Tier 2/3 markets, where SME digitization is still ramping.

Management Commentary (Simplified)

- They are leaning on their first-mover brand, deep listings, and a scalable tech stack to keep monetizing local search.

- Focus remains on improving advertiser ROI via better placements, richer profiles, and ratings – to boost renewals and upgrades.

- Investments in product (JD Mart, Omni, Xperts) and sales reach are near-term costs intended to widen the long-term opportunity.

- Prepaid model and disciplined execution are positioned as strengths for predictable cash flows.

Key Positives

- Large, sticky ecosystem: 54.7m listings and 157.1m reviews create network effects and defensibility.

- Monetization base intact with 631k+ active paid campaigns; add-ons provide ARPC upside.

- Mobile-led traffic (85.7%) supports scale with relatively low incremental cost per user.

- Prepaid model generally means lower receivable risk and healthier cash conversion vs. typical ad businesses.

- Broad on-ground coverage across India positions the firm well for SME digitization in smaller cities.

Key Concerns

- Q/Q traffic dip (↓) needs monitoring; repeated softness could pressure lead volumes and renewals.

- Intense competition from search platforms and maps could cap pricing power or increase acquisition costs.

- SME ad budgets are cyclical; macro weakness can raise churn or push downgrades.

- Newer initiatives (JD Mart, Omni, Xperts) carry execution risk and may weigh on margins before scale.

- Limited visibility on exact quarterly financials in the deck; investors should watch the official results release for revenue, ARPC, margin and cash metrics.

Final Takeaway for Investors

Just Dial remains a high-reach, mobile-first local discovery platform with a sizable monetization base and a cash-friendly prepaid model. The slight Q/Q traffic dip makes the next couple of quarters important: investors should look for stabilization or re-acceleration in visitors, growth in active paid campaigns and ARPC, and clarity on margin trajectory as sales and product investments continue. Long-term story is intact, but near-term performance will hinge on execution and competitive dynamics.

FAQs

- What is revenue?

Revenue is the money the company earns from advertisers (mostly SMEs) who pay for listings, premium placements, and add-on services like banners, website builder, JD Pay, and ratings tools. - What is profit?

Profit is what remains after subtracting all expenses (sales, marketing, employee costs, technology, server/infra, admin, taxes, etc.) from revenue. It shows how efficiently the company turns sales into earnings. - Why did profit change?

Even if revenue is steady, profit can move due to spending on sales hiring, marketing, product development, technology depreciation, provisions/write-offs, or tax adjustments. One-time items can also swing profit temporarily. - Is this a good stock?

It depends on your risk profile. Positives include scale, prepaid model, and mobile-first usage. Key watch-outs are traffic trends, competition, and execution in new products. Review the official results (revenue, margins, cash) and your investment horizon before deciding. - How does Just Dial grow revenue?

By adding more paid advertisers, improving renewal rates, upselling higher-tier packages and add-ons, and expanding into new categories and geographies (including Tier 2/3 markets).

Disclaimer

This post is for educational purposes only and is not investment advice. Figures referenced are from the company’s April 2026 investor materials where available; please read the official results and consult a financial advisor before making investment decisions.