Quick Summary: Angel One Results

- Audited Q4 FY26 and FY26 results approved; auditor gave an unmodified opinion (clean report) ↑

- Raised Rs 50 crore via NCDs in Q4; plans to raise up to Rs 1,500 crore more through NCDs ↑

- Borrowing limits increased to Rs 20,000 crore (subject to shareholders) for strategic flexibility ↑

- Investing Rs 150 crore each into Angel Fincap (lending) and Angel One Wealth (wealth) to scale new engines ↑

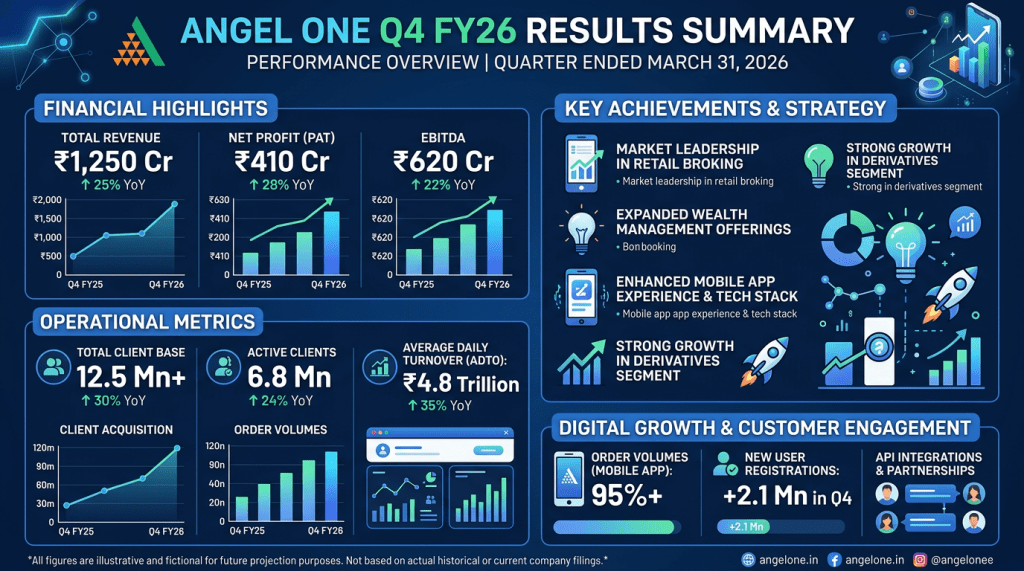

Angel One Financial Highlights

Note: The company approved the audited standalone and consolidated results for Q4 FY26 and FY26, but the numbers were not included in the exchange text shared. Here are the headline actions with confirmed amounts and dates:

- Period covered: Q4 FY26 and FY26 (audited)

- Audit outcome: Unmodified opinion from statutory auditor (clean report)

- Debt raised in Q4: Rs 50 crore via Non-Convertible Debentures (private placement)

- Planned debt raise: Up to Rs 1,500 crore NCDs (in one or more tranches, private placement)

- Borrowing headroom: Increased to Rs 20,000 crore under Sections 180(1)(c), 180(1)(a), and 186 (subject to shareholder approval)

- Equity infusion into subsidiaries:

- Rs 150 crore into Angel Fincap Private Limited (wholly owned)

- Rs 150 crore into Angel One Wealth Limited (wholly owned)

- Security cover: Statement filed as of March 31, 2026

- Internal auditor: KPMG Assurance and Consulting Services LLP appointed for FY27

- AGM: To be held on June 12, 2026 via virtual mode

Why Key Numbers Changed (Important Insight)

Without the detailed P&L, here’s how to think about the likely drivers and what to check when the full results PDF is out:

- Broking activity and market volumes:

- Revenue tends to rise with higher equity/F&O turnover and active client adds ↑.

- If market volatility was lower, order flows and brokerage yields can soften ↓.

- Product mix effects on margins:

- More F&O and MTF (margin trade funding) usually lifts activity but can pressure blended yields ↓.

- Rising distribution/wealth fees are margin-accretive ↑.

- Interest income vs finance costs:

- Lending/Margin funding income scales with book size and rates ↑.

- New NCDs increase interest expense; net impact depends on spread (lending yield minus cost of funds).

- Operating costs:

- Tech, cloud, and compliance costs tend to rise as the platform scales ↓ for margins.

- Marketing spends swing with client acquisition campaigns.

- Profit vs revenue:

- Revenue is all income (brokerage, interest, distribution fees, etc.).

- Profit is what remains after costs (employee, tech, finance costs, taxes). Profit can fall even if revenue rises, if costs/finance charges rise faster.

- One-time items:

- The auditor’s unmodified opinion suggests no major red flags. If any exceptional gains/losses exist (e.g., provisions, write-offs), they’ll be in the notes to accounts.

- Margin changes to watch:

- EBITDA margin: Sensitive to product mix (broking vs wealth) and operating leverage.

- PAT margin: Also influenced by finance costs as debt increases.

Operational Performance & Business Trends

- Broking platform scale: Core engine remains retail broking (equities and F&O). Client growth, activation, and average daily turnover (ADTO) will drive the top line.

- Lending expansion (Angel Fincap): The Rs 150 crore infusion plus higher borrowing headroom point to scaling margin funding/secured lending. This can lift interest income but adds credit and market risk management needs.

- Wealth build-out (Angel One Wealth): Another Rs 150 crore supports advisory, distribution, and potentially PMS/solutioning. Wealth fees are stickier and can smooth earnings across market cycles.

- Funding strategy: The existing Rs 50 crore NCD and an enabling limit of up to Rs 1,500 crore give balance-sheet flexibility to fund loan book growth and platform investments.

- Governance & controls: Appointing KPMG as internal auditor for FY27, and filing the security cover statement, signal a tighter control environment as leverage scales.

Management Commentary (Simplified)

- We want flexibility: Increasing borrowing limits to Rs 20,000 crore gives room to fund growth when needed, without repeated approvals.

- Diversify beyond broking: Capital into lending and wealth aims to build multiple revenue streams and deepen client monetization.

- Strengthen controls: Bringing in KPMG for internal audit underscores focus on governance as the business mix gets more complex.

- Raise when markets allow: Enabling a larger NCD program lets the company time issuances to cost-effective windows.

Key Positives

- Clean audit (unmodified opinion) reduces uncertainty around reported numbers.

- Strategic investments into lending and wealth can raise lifetime value per client and smooth cyclicality.

- Funding optionality via Rs 1,500 crore NCD plan and Rs 20,000 crore borrowing limit supports scale-up.

- Governance upgrade with KPMG as internal auditor aligns with a larger, more leveraged balance sheet.

Key Concerns

- Leverage and cost of funds: More NCDs mean higher interest expense; spreads must be preserved.

- Regulatory risk: Any SEBI changes to F&O or margin norms can impact volumes and funding income.

- Credit/market risk in lending: Rapid growth in margin funding needs strong risk management and provisioning.

- Execution complexity: Running broking, lending, and wealth in tandem raises operational and compliance demands.

Final Takeaway for Investors

Angel One is signaling a clear move from a transaction-led broker to a diversified retail financial platform. The clean audit is comforting, and the capital roadmap—NCDs, higher borrowing headroom, and equity into subsidiaries—suggests confidence in scaling lending and wealth. The flip side is leverage: finance costs will rise, and risk governance must keep pace. Wait for the detailed FY26 numbers (revenue, PAT, margins, client metrics) to judge execution quality, but the direction of travel is clear—broader, more annuity-like earnings, with tighter risk controls needed.

FAQs

- What is revenue?

- Revenue is the total income a company earns from its operations—brokerage, interest from lending/margin funding, distribution and wealth fees, and other charges.

- What is profit?

- Profit is what remains after subtracting operating costs, employee expenses, technology costs, finance costs, depreciation, and taxes from revenue.

- Why did profit change if revenue moved differently?

- Profit can rise or fall faster than revenue due to changes in product mix, operating leverage, finance costs from new debt, and any one-time items or provisions.

- What does increasing borrowing limits to Rs 20,000 crore mean?

- It’s an enabling approval. It doesn’t mean the company will borrow the full amount immediately, but it gives flexibility to raise debt as growth opportunities arise.

- Is Angel One a good stock after these results?

- The strategic direction looks positive (diversification and funding flexibility). However, assess the detailed FY26 numbers, spreads in lending, client growth/ADTO trends, and risk controls before making a decision. Consider your risk profile and time horizon.

Disclaimer

This post is for educational purposes only.