Quick Summary: Anand Rathi Results

- ↑ FY26 revenue up 22% to ₹1,198 Cr; PAT up 28% to ₹386 Cr; PAT margin improved by ~215 bps to 32.2%.

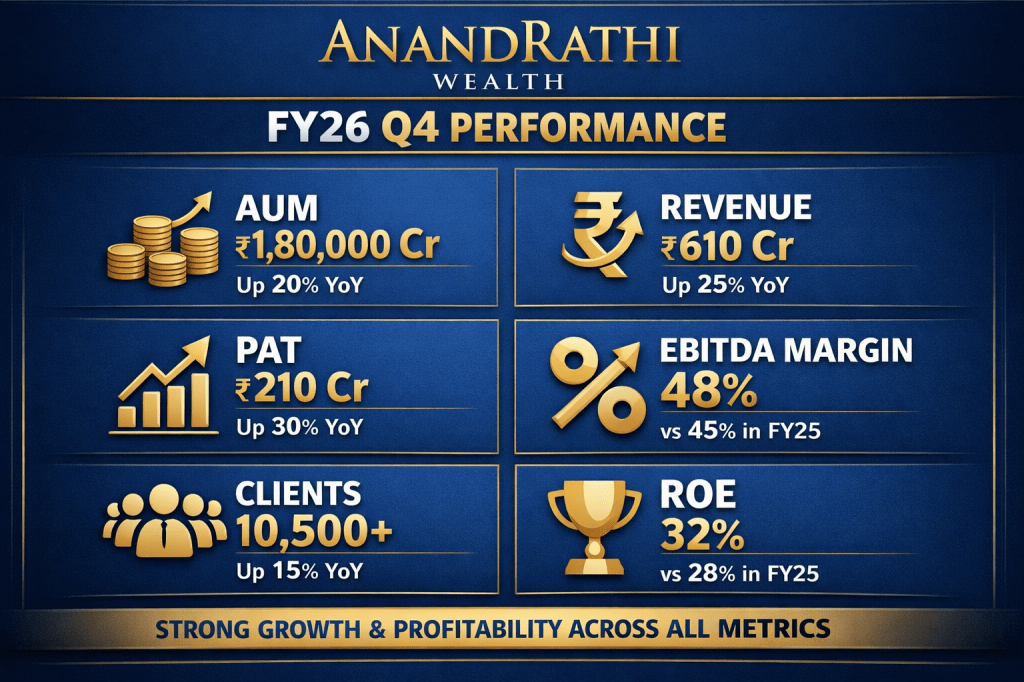

- ↑ Q4 FY26 revenue at ₹302 Cr (+25% y/y); PAT at ₹92 Cr (+21% y/y).

- ↑ AUM rose 25% y/y to ₹93,037 Cr; equity MFs still >50% of mix; debt share inched up.

- Stronger franchise metrics: RMs up to 401; active client families at 13,395; AUM per RM up to ₹226 Cr; regret RM attrition at ~10%.

Anand Rathi Financial Highlights

– FY26 (consolidated; core view):

– Total revenue: ₹1,198 Cr (FY25: ₹980 Cr)

– PAT: ₹386 Cr (FY25: ₹301 Cr)

– PAT margin: 32.2% (FY25: 30.7%)

– ROE (annualized): 46.7% (FY25: 44.6%)

– Q4 FY26 (consolidated; core view):

– Total revenue: ₹302 Cr (Q4 FY25: ₹241 Cr)

– PAT: ₹92 Cr (Q4 FY25: ₹74 Cr)

– AUM: ₹93,037 Cr (Mar-26) vs ₹77,103 Cr (Mar-25), up 25%

– Product mix (AUM share; Mar-26 vs Mar-25):

– Equity MF: ~51% (was ~53%)

– Debt MF: ~16% (was ~14%)

– Structured products: ~5% (flat)

– Others: ~28% (flat)

– Franchise metrics (Private Wealth):

– Relationship Managers (RMs): 401 (was 380)

– Active client families: 13,395 (was 11,732)

– AUM per RM: ₹226 Cr (was ₹198 Cr)

– Clients per RM: 33 (was 31)

Note: FY26 and Q4 FY26 “core” results exclude fair value gains on investments of ₹54.6 Cr, ESOP expenses of ₹39.3 Cr, and related tax effects of ₹3.8 Cr (ROE shown as reported).

Why Key Numbers Changed (Important Insight)

- Revenue growth: Higher market levels (mark-to-market gains on client portfolios) plus steady net equity MF inflows lifted fee pools. A higher wallet share from HNI clients and healthy annuity trails (SIP/recurring fees) supported double-digit topline growth.

- Profit grew faster than revenue: Operating leverage kicked in as costs grew slower than AUM/fees. Productivity improved (AUM per RM up), and a stable mix of advisory/managed products sustained yields—together pushing PAT ahead of revenue.

- Margin expansion: PAT margin improved ~215 bps to 32.2% on scale benefits and disciplined costs. A small tilt toward debt MFs could have been a headwind to yield, but this was offset by higher overall AUM and better monetization.

- One-time/adjusted items: Management excluded fair value gains (₹54.6 Cr) and ESOP expenses (₹39.3 Cr) plus related taxes to present the underlying operating performance. Fair value gains are non-operating and volatile; ESOP cost is non-cash but recurring—excluding both gives a “core” view. Reported profit would differ if these were included.

- ROE uplift: Strong profit growth with a relatively light balance sheet (fee-led model) drove ROE to 46.7%, among the best in domestic wealth management.

Operational Performance & Business Trends

Anand Rathi’s model is relationship-led, not capital-heavy. That shows up in the metrics. More RMs, higher AUM per RM, and more clients per RM indicate better capacity utilization. The client base continues to shift up-market:

– AUM contribution is increasingly from HNIs/UHNIs: ~50% of AUM now sits in the ₹5–50 Cr segment, and ~28.9% is ₹50 Cr+, up sharply from 2021 levels. This “move up the curve” boosts stickiness and long-term share of wallet.

– Equity MFs remain the anchor (>50% of AUM), but debt’s share ticked up, which diversifies risk. Even with a slightly lower equity mix, AUM tailwinds from market performance and net inflows supported fees.

– RM franchise quality is stable: regret RM attrition fell to ~10%, and the firm retained ~75% of AUM from a handful of high-tenure RMs who exited—underscoring client stickiness to the platform, not just individuals.

– Market share in equity MF net inflows is inching up, aided by improving mark-to-market and steady gross sales, which sets the stage for gradual share gains.

Management Commentary (Simplified)

– Wealth management is a credibility and trust marathon, not a capital sprint. The firm prioritizes transparency on earnings with clients and avoids product “manufacturing” risks until the distribution base is strong.

– Leaders are hands-on RMs, keeping the organization close to clients and execution. Aggressive hiring alone doesn’t build a franchise; capability-building and stable incentives do.

– Focus stays on HNIs/UHNIs where relationships are deeper and the business is more sustainable. Consistent ROE and shareholder payouts (dividends/buybacks/bonuses) remain priorities.

– The company presented FY26 on a core basis (excluding fair value gains and ESOP cost) and is guiding for continued growth on the same core logic.

Key Positives

- Strong FY26 print: revenue +22%, PAT +28%, margin expansion.

- AUM up 25% to ₹93,037 Cr with improving productivity per RM.

- High-quality franchise: ROE at 46.7%, low regret RM attrition, rising wallet share from HNIs/UHNIs.

- Sticky annuity elements (trails/SIPs) and improving market share in equity MF flows support visibility.

- Clear discipline around one-offs and transparency—better read-through of core earnings quality.

Key Concerns

- Market-linked revenues: Prolonged equity corrections could slow AUM/fee growth.

- Product mix: A lower equity share can dilute yields; structured products need tight risk controls.

- Talent intensity: Business depends on RM quality; any spike in RM churn can disrupt near-term flows.

- Regulatory risk: Changes to distribution commissions or disclosure norms could impact margins.

- ESOP expense and fair-value items can create noise between reported and “core” earnings—investors must track both.

Final Takeaway for Investors

Anand Rathi Wealth delivered a clean, growth-heavy FY26 with better margins, strong ROE, and rising AUM. The franchise is moving up-market with healthier client stickiness and RM productivity. While the model is inherently market-sensitive and people-dependent, execution quality looks solid. For long-term investors tracking India’s wealth creation theme, this remains a credible compounding story—best approached with awareness of market cycles and careful attention to core vs reported earnings.

FAQs

- What is “revenue” here?

Revenue is the fee income and related operating income the firm earns from managing and advising client wealth (distribution, advisory, and associated services). - What is “profit” (PAT)?

PAT is Profit After Tax—the net earnings left after all operating expenses, interest, depreciation, and taxes. - Why did profit grow faster than revenue?

Operating leverage (costs rising slower than fees), a better client/product mix, and higher AUM per RM lifted margins—so PAT rose faster than the topline. - What is AUM and why does it matter?

AUM (Assets Under Management) is the total client assets the firm advises/manages. Higher AUM generally means higher fee potential and earnings visibility. - Is this a good stock to buy?

It’s a strong franchise with high ROE and solid execution. However, it is market- and talent-sensitive. Assess valuation, your risk tolerance, and portfolio fit before deciding. This is not investment advice.

Disclaimer

This post is for educational purposes only and is not investment advice. Figures are based on the company’s investor materials; FY26 and Q4 FY26 core results exclude fair value gains, ESOP expenses, and related tax effects as disclosed by the company. Always do your own research or consult a licensed advisor before investing.