Tata Motors has once again delivered a stable quarterly performance in Q1 FY25-26, showcasing its strength and discipline despite facing multiple global hurdles. The company’s ability to maintain profits in the face of regulatory changes, foreign exchange volatility, and sector-wide headwinds reflects its resilient strategy and operational maturity.

📊 Financial Snapshot – Q1 FY26

| Metric | Q1 FY26 | Q1 FY25 | YoY Trend |

|---|---|---|---|

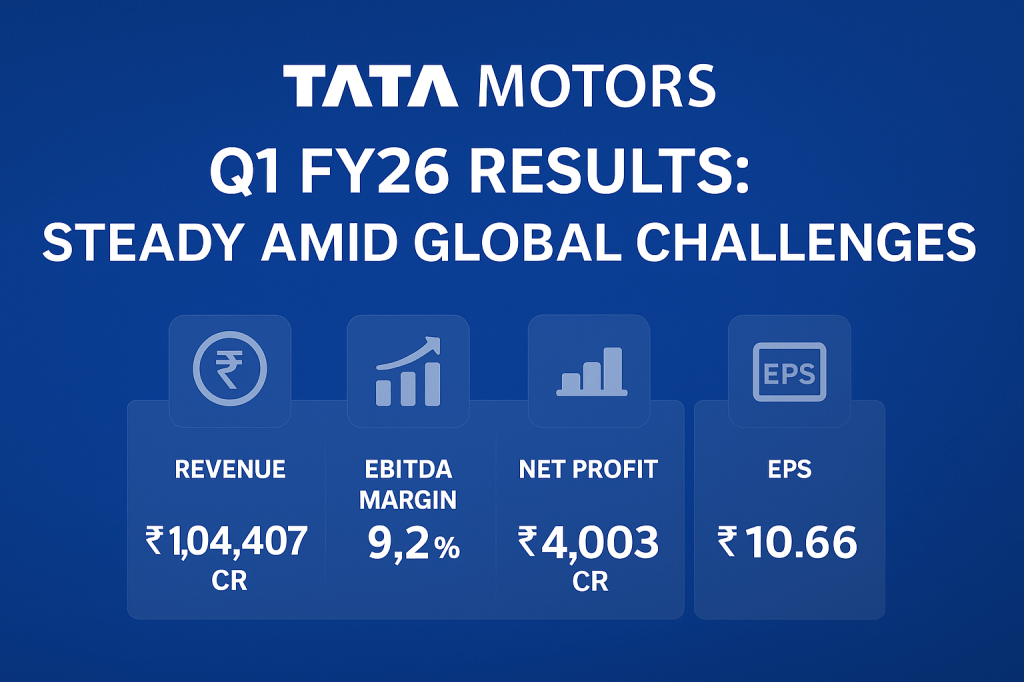

| Operating Revenue | ₹1,04,407 Cr | ₹1,07,102 Cr | ↓ 2.5% |

| EBITDA Margin | 9.2% | 14.0% | ↓ 480 bps |

| Profit Before Tax | ₹5,561 Cr | ₹8,894 Cr | ↓ 37.5% |

| Net Profit | ₹4,003 Cr | ₹10,587 Cr | ↓ 62% |

| Earnings Per Share (EPS) | ₹10.66 | ₹27.41 | ↓ 61% |

🌐 Tackling Global Disruptions Head-On

🇺🇸 US Tariffs Hit JLR

- The steep 27.5% tariff on UK vehicle exports to the US led to an extra cost of ₹2,904 Cr in Q1.

- Despite this, Tata Motors still reported a respectable ₹4,003 Cr in profit, a clear sign of adaptability.

📉 Currency Volatility & Economic Uncertainty

- JLR’s Q1 revenue dropped to £6.6 billion due to shipping delays and a planned phase-out of older models.

- However, margins were kept within guidance levels, thanks to better pricing and operational control.

🚗 Segment-Wise Breakdown

🚛 Commercial Vehicles (CV)

- Revenue: ₹17,009 Cr | EBIT Margin: 9.7%

- Maintained leadership in domestic market share

- Introduced innovations like Ace Pro EV and air-conditioned truck cabins

- ROCE stood strong at ~40%, indicating efficient capital usage

🚗 Passenger Vehicles (PV + EV)

- Revenue: ₹10,877 Cr | EBIT Margin: -2.8%

- PV segment faced demand softness, especially in entry-level models

- EV business remains the growth engine:

- Achieved 40% VAHAN market share in July 2025

- Strong bookings for Harrier.ev and growing interest in Nexon.ev

🌍 Jaguar Land Rover (JLR)

- Revenue: £6.6B | EBIT Margin: 4.0%

- Tariff pressure and currency headwinds were partially offset by improved operational efficiencies

- Despite challenges, the company maintained over £5B in liquidity and continued investing in next-gen vehicles

💼 Strengthening the Foundation

- ✅ Tata Motors is moving ahead with the demerger of Tata Finance, effective from Oct 1, 2025

- ✅ The acquisition of IVECO (excluding defense business) is in progress, set to enhance global presence

- ✅ Continued focus on electric mobility, premium vehicle launches, and smart logistics solutions

💰 Financial Metrics Overview

| Metric | Q1 FY26 | Q1 FY25 |

|---|---|---|

| Debt-to-Equity | 0.48 | 0.71 |

| Free Cash Flow | ₹(3,800) Cr | ₹700 Cr |

| Net Profit Margin | 3.83% | 9.88% |

The negative cash flow this quarter is primarily due to seasonal working capital needs and inventory buildup—a temporary and expected outcome.

📈 Shareholding Trends – Q1 FY26

| Category | Holding | Change |

|---|---|---|

| Promoters | 46.37% | No Change |

| Foreign Investors (FII) | 16.93% | ↓ 0.42% |

| Domestic Institutions (DII) | 21.74% | ↑ 0.38% |

| Public & Retail | ~14.96% | Stable |

🧠 Insight: While foreign institutions slightly trimmed their stakes due to global uncertainties, domestic mutual funds and insurers increased their exposure, reaffirming confidence in Tata Motors’ growth story.

🔎 Final Thoughts: Resilience Backed by Strategy

Tata Motors’ Q1 FY26 performance confirms that consistency in challenging times is a bigger achievement than growth in stable conditions. Whether navigating trade barriers, adapting product lines, or accelerating EV adoption—Tata Motors is clearly on a long-term transformation path.

📢 Key Positives for Long-Term Investors:

- Rising share in the EV market

- Structurally improving balance sheet

- Strategic global expansion (IVECO deal, demerger)

- Strong domestic brand power in both PV and CV

🌍 Stay Updated

For more market updates and SME stock insights, follow us on:

👉 YouTube – @stock3727

👉WordPress – https://stockresult.in/posts-page/

Enjoyed this post? Like, Comment & Follow my blog for more insightful content!