RBL Bank reported a steady quarter. Revenue inched up, profit improved sequentially, and asset quality strengthened. Costs remain high, and the retail business is still loss-making, but losses narrowed. Overall, the bank looks more stable than a year ago, with cleaner books and healthier returns.

Quick Summary: RBLBANK Results

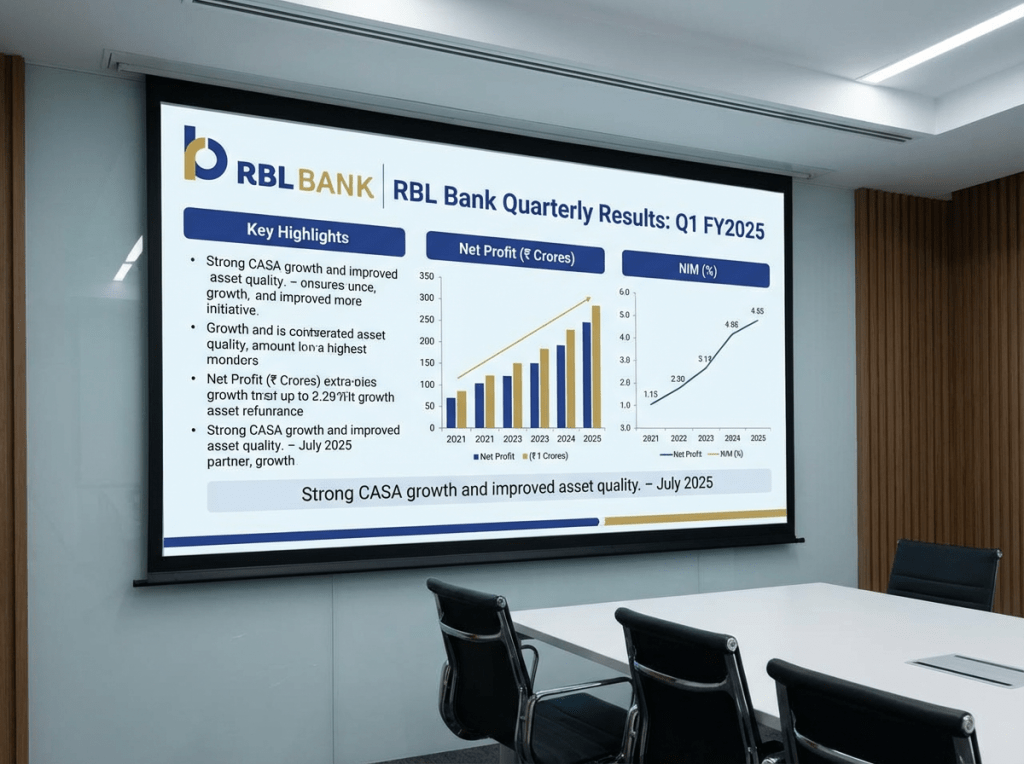

- Q3 FY26 PAT at Rs 214 crore (↑ QoQ 20%; strong rebound YoY from a low base) 🙂

- NII at Rs 1,657 crore (↑ QoQ 7%; ↑ YoY 5) on better loan yields vs funding cost

- Asset quality improved: GNPA 1.88% (↓ from 2.32% QoQ), NNPA 0.55%

- Provisions Rs 639 crore (↑ QoQ; ↓ YoY 46%)—credit costs normalize QoQ, much lower than last year

- Capital adequacy (Basel III) at 14.47% (↓ marginally QoQ), RoA annualised at 0.55%

RBLBANK Financial Highlights

All numbers are standalone; Rs crore unless stated.

- Total income (Q3 FY26): 4,717 (↑ QoQ 6%; ↑ YoY 2%)

- Net Interest Income (NII): 1,657 (↑ QoQ 7%; ↑ YoY 5%)

- Other income: 1,050 (↑ QoQ 13%; ↓ YoY 2%)

- Operating expenses: 1,795 (↑ QoQ 2%; ↑ YoY 8%)

- Pre-provision operating profit (PPOP): 912 (↑ QoQ 25%; ↓ YoY 9%)

- Provisions and contingencies: 639 (↑ QoQ 28%; ↓ YoY 46%)

- Profit before tax: 273 (↑ QoQ 19%; vs loss YoY)

- Profit after tax (PAT): 214 (↑ QoQ 20%; vs Rs 33 crore YoY)

- EPS (basic): Rs 3.48 (vs Rs 2.92 QoQ; Rs 0.54 YoY)

- Cost-to-income (approx.): 66% (better vs ~71% QoQ; weaker vs ~63% YoY)

- GNPA/NNPA: 1.88%/0.55% (vs 2.32%/0.57% QoQ)

- Capital Adequacy Ratio: 14.47% (vs 14.71% QoQ; 14.86% YoY)

- 9M FY26: Total income Rs 13,668 crore (↑ 2% YoY); PAT Rs 593 crore (↓ 5% YoY) as operating profit fell and taxes normalized

Why Key Numbers Changed (Important Insight)

- Profit vs revenue: Revenue grew modestly, but profit rose faster QoQ because PPOP expanded and asset quality improved, even after higher provisions. YoY, profit jumped mainly because last year had very high credit costs.

- Margins: NII improved as asset yields stayed firm and deposit costs were contained, lifting core income. The cost-to-income ratio eased QoQ (better operating leverage) but is still higher than last year, reflecting ongoing spend on people, tech, and distribution.

- Provisions: QoQ increase reflects normalized credit costs and conservative buffers; YoY drop is large because Q3 last year saw heavy stress recognition and provisioning. This base effect is a big driver of the YoY PAT jump.

- Other income: Sequential rise (fees/treasury/other banking income were stronger), while YoY was broadly stable to slightly lower, indicating less reliance on volatile gains vs last year.

- Taxes and one-time items: No exceptional items reported. Tax expense normalized this quarter, unlike the YoY comparison where a prior tax credit had distorted the base.

Operational Performance & Business Trends

- Corporate/Wholesale banking: Profit before tax at Rs 199 crore (steady QoQ; stronger YoY). This book appears to be pulling its weight with stable spreads and lower slippages.

- Retail banking: Still in loss at Rs -95 crore, but losses narrowed materially QoQ and sharply YoY. The drag is reducing—helped by better collections and tighter underwriting.

- Treasury: Swung back to a profit of Rs 93 crore vs a small loss last quarter; lower YoY compared to a stronger base. This line remains inherently volatile with rate movements.

- Other banking operations: Profit at Rs 76 crore, up QoQ and YoY—steady support from payments/fee businesses.

- Asset quality: GNPA fell to 1.88% (from 2.32% QoQ), and gross NPAs by value also declined. NNPA stayed low at 0.55%, indicating adequate provisioning.

Management Commentary (Simplified)

- The filing focused on numbers, without detailed qualitative commentary. Reading the trends, the bank appears to prioritize asset quality and disciplined growth, while continuing investments in people and technology.

- Capital remains comfortable at 14.47%, giving room for growth, though it is slightly lower QoQ—consistent with balance-sheet expansion and risk-weight changes.

- The path to improved profitability seems to hinge on three levers: sustaining NII growth, keeping credit costs in check, and tightening operating efficiency.

Key Positives

- Sharp improvement in asset quality (GNPA down to 1.88%); healthier book

- NII growth and better operating leverage QoQ; PPOP up 25%

- Provisions much lower YoY, supporting a cleaner earnings profile

- Retail losses narrowing—profit path looks more credible if this trend continues

- RoA improved to 0.55% annualised; EPS recovery visible

Key Concerns

- Cost-to-income still elevated (~66%); efficiency needs to improve further

- Capital ratio dipped to 14.47%; adequate but trending slightly lower

- Retail segment remains loss-making; sustained profitability requires further improvement in collections and risk costs

- Provisions rose QoQ; any macro slowdown or retail stress can push credit costs up

- Treasury income volatility can swing quarterly earnings

Final Takeaway for Investors

RBL Bank delivered a cleaner, more stable quarter. Profits improved QoQ, asset quality strengthened, and the retail drag is reducing. The big YoY jump in profit is helped by a weak base, so the true test is sustaining PPOP growth while bringing down the cost-to-income ratio. With capital adequate and credit costs normalizing, the direction of travel is positive—but consistent retail profitability and tighter cost control are the key milestones to watch in coming quarters.

FAQs

- What is revenue (total income) for the quarter? Total income was about Rs 4,717 crore in Q3 FY26, including interest income and other income like fees and treasury gains.

- What is profit for the quarter? Profit after tax (PAT) was about Rs 214 crore in Q3 FY26.

- Why did profit change this quarter? Profit rose mainly due to better core income and improved asset quality. Provisions were higher than last quarter but far lower than last year’s heavy credit costs. Costs stayed high, but operating leverage improved QoQ.

- How are margins? NII grew ~7% QoQ and ~5% YoY, indicating firmer spreads. The cost-to-income ratio improved QoQ to ~66%, though it remains higher YoY.

- Is RBL Bank a good stock to buy now? The trend is improving, especially on asset quality and earnings stability. That said, elevated costs and loss-making retail still need work. Investors should track cost efficiency, retail profitability, and credit costs before making decisions, and consider their own risk profile.

Disclaimer

This post is for educational purposes only. It is not investment advice. Please do your own research or consult a SEBI-registered advisor before investing.