India’s largest life insurer, Life Insurance Corporation of India (LIC), announced its Q1 FY25-26 results on August 7, 2025. The performance marks a steady stride toward profitability, business mix transformation, and operational efficiencies. Let’s dive into what this means for investors.

📊 Key Financial Highlights

| Metric | Q1 FY26 | Q1 FY25 | YoY Change |

|---|---|---|---|

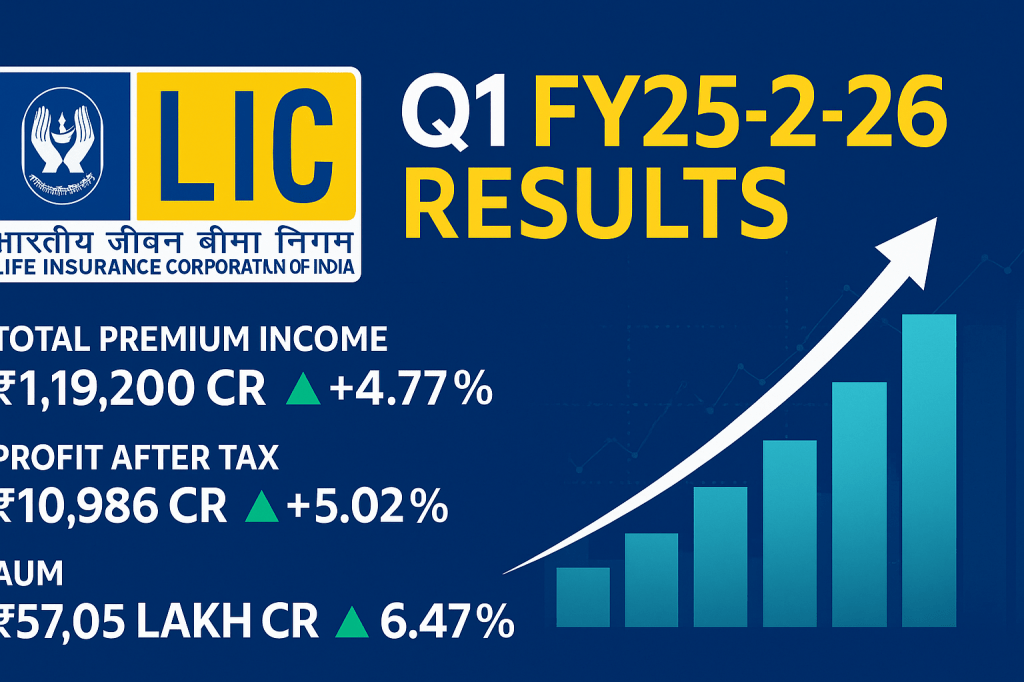

| Total Premium Income | ₹1,19,200 Cr | ₹1,13,770 Cr | 🔼 4.77% |

| Profit After Tax (PAT) | ₹10,986 Cr | ₹10,461 Cr | 🔼 5.02% |

| Assets Under Management (AUM) | ₹57.05 Lakh Cr | ₹53.59 Lakh Cr | 🔼 6.47% |

| Net VNB (Value of New Business) | ₹1,944 Cr | ₹1,610 Cr | 🔼 20.75% |

| VNB Margin | 15.4% | 13.9% | 🔼 1.5% (Absolute) |

| Solvency Ratio | 2.17 | 1.99 | ✅ Healthy |

🧾 Segment Performance Insights

- Individual New Business Premium rose to ₹12,536 Cr (↑ 5.42%)

- Group Business Premium increased to ₹47,726 Cr (↑ 2.46%)

- Renewal Premiums touched ₹58,938 Cr (↑ 6.58%)

- Total Death Claims Paid stood at ₹6,824 Cr

- Maturity Claims Paid surged to ₹50,584 Cr (↑ 20.57%)

🏦 Shareholding Pattern (As of June 30, 2025)

- 👨💼 Promoter (Government of India): 96.50%

- 🌍 Foreign Institutional Investors (FIIs): ~1.3%

- 🏛 Domestic Institutional Investors (DIIs): ~1.2%

- 📢 Public Shareholding: ~1.0%

Despite being a publicly listed company, the government retains a majority stake, which ensures long-term strategic control and market trust.

🚀 Business Transformation in Motion

LIC’s strategy is clearly visible:

- Non-Participating (Non-Par) Business share in APE improved from 23.94% to 30.34%

- Persistency Ratios across all policy terms improved, reflecting better customer retention

- Digital Push via ANANDA App and WhatsApp services enhanced agent productivity and customer experience

- Bancassurance Channel nearly doubled YoY (↑ 98.23%)

These factors contributed to a noticeable margin boost and more stable earnings.

📉 Market Share and Areas of Concern

- LIC’s market share by policy count fell slightly to 63.07% from 66.54% last year

- Claim settlement ratio also dipped to 94.59% (from 96.32%)

While these are not alarming, they indicate rising competition from private players and demand continued vigilance.

📈 What Should Investors Do?

✅ Positives

- Strong embedded value at ₹7.77 lakh crore (↑ 6.81% YoY)

- Rising VNB margin points to improved product mix

- Operational cost efficiencies are visible in falling expense ratios

- Solvency remains above regulatory norms

⚠️ Things to Watch

- Any future stake dilution by the government

- Competitive pricing and innovation from private insurers

- Further digital adoption and customer onboarding experience

🧠 Final Thoughts

LIC is not just a traditional insurer anymore — it’s evolving into a digitally aware, cost-efficient, and profit-focused institution. With steady premium growth, a strong rural footprint, and a growing non-par portfolio, LIC is positioning itself well for long-term investors.

If you’re a long-term investor looking for stability, insurance-sector exposure, and steady dividends (when declared), LIC deserves your attention — especially at current valuation levels where it’s still catching up with private peers.

🌍 Stay Updated

For more market updates and SME stock insights, follow us on:

👉 YouTube – @stock3727

👉WordPress – https://stockresult.in/posts-page/

Enjoyed this post? Like, Comment & Follow my blog for more insightful content!