Meta Description:

MobiKwik Q4 FY25 results show strong growth in digital payments and user base, but profitability takes a hit due to weak lending business. Read the full financial analysis and investor outlook.

🧾 MobiKwik Q4 FY25 Financial Results – Summary at a Glance

India’s leading digital wallet and fintech platform, MobiKwik, reported its Q4 FY25 earnings with mixed results. The company showcased a massive jump in transaction volumes and user growth, yet faced a steep drop in profitability due to underperformance in its lending segment.

🔍 Key Quarterly Highlights (Q4 FY25 vs Q4 FY24)

| Metric | Q4 FY25 | Q4 FY24 | YoY Change |

|---|---|---|---|

| Revenue from Operations | ₹267.8 Cr | ₹264.9 Cr | ▲ 1.1% |

| Total Income | ₹278.5 Cr | ₹271.6 Cr | ▲ 2.5% |

| EBITDA | ₹(45.8) Cr | ₹5.9 Cr | ▼ Negative Turn |

| Net Profit (Loss) | ₹(56.0) Cr | ₹(0.7) Cr | ▼ Steep Decline |

| Contribution Margin | 22.8% | 36.0% | ▼ Lowered |

📈 Full-Year FY25 Performance – Strong Revenue, Weak Margins

| Metric | FY25 | FY24 | YoY Change |

|---|---|---|---|

| Revenue from Operations | ₹1,170.2 Cr | ₹875.0 Cr | ▲ 33.8% |

| Total Income | ₹1,192.5 Cr | ₹890.3 Cr | ▲ 34.0% |

| EBITDA | ₹(79.4) Cr | ₹37.2 Cr | ▼ Losses Incurred |

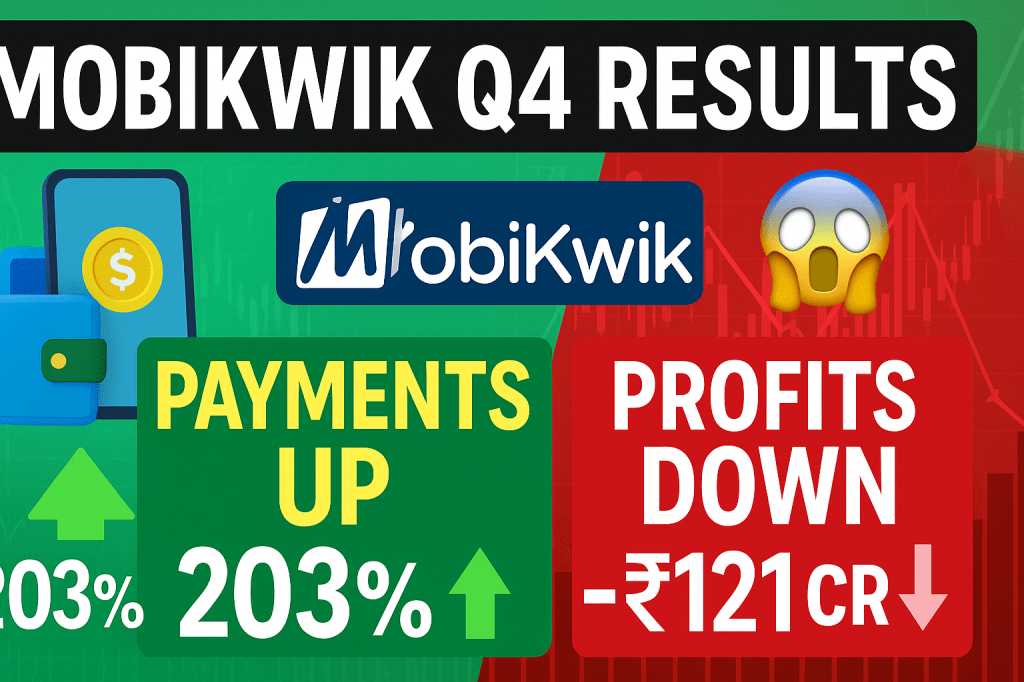

| Net Profit (Loss) | ₹(121.5) Cr | ₹14.1 Cr | ▼ Reversal |

| Payments GMV | ₹1,15,868 Cr | ₹38,195 Cr | ▲ 203% |

| Credit Disbursement (GMV) | ₹5,358 Cr | ₹9,093 Cr | ▼ 41% |

💳 Segment-Wise Performance Breakdown

✅ Digital Payments

- Transaction volumes (GMV) grew over 200% YoY.

- Payments revenue increased 142% YoY to ₹767.4 Cr.

- Gross Margin rose to 19.7%, among the best in industry.

- Registered user base grew to 17.64 Cr with 2.06 Cr new users in FY25.

🔻 Digital Credit & Lending

- Credit disbursements fell sharply by 41% YoY.

- Despite lower volumes, margins in lending improved slightly (46.7% vs 45.7% last year).

- Lending costs increased, driven by accounting changes and paused short-tenure products.

🔬 Balance Sheet Overview (As of March 31, 2025)

| Item | FY25 (₹ Cr) | FY24 (₹ Cr) |

|---|---|---|

| Total Assets | ₹1,360.4 | ₹854.7 |

| Shareholder Equity | ₹588.7 | ₹162.6 |

| Total Liabilities | ₹771.7 | ₹692.1 |

| Cash & Equivalents | ₹276.6 | ₹294.6 |

👥 Ownership & IPO Utilization Insights

- MobiKwik went public in Dec 2024, raising over ₹530 Cr through IPO.

- IPO Proceeds are still largely unutilized: ~₹3,800 Cr remains available for growth.

- No major changes observed in promoter or institutional shareholding as per recent filings.

🧠 Strategic Growth Outlook

🔹 Innovation-Focused Expansion

- AI-based tools to improve collections, agent productivity, and coding cycles.

- Launch of Pocket UPI – a bank-free UPI alternative focused on Bharat.

- Rollout of FD-backed credit card to drive first-time credit access.

🔹 Fintech Ecosystem Play

- Introducing B2B products: in-chat payments, instant settlements, and EMI stack at checkout.

- Exploring new lending partnerships and secured credit options for H2 FY26.

🤖 Expert Verdict: Buy, Hold or Avoid?

🔼 Positives:

- Explosive payments growth (GMV up 203%)

- Cost-efficient operations with rising gross margins

- Diversifying fintech product lines with UPI-first and AI-led tools

🔽 Negatives:

- Net losses widened in FY25 to ₹121.5 Cr

- Digital credit volumes dropped over 40%

- EBITDA margin turned negative (-6.7%) due to fixed costs and lending headwinds

📌 Final Words:

MobiKwik is clearly growing, especially in the digital payments space. However, until the lending business revives and margins stabilize, the stock remains risky for short-term investors but potentially rewarding for long-term believers in India’s fintech story.

Disclaimer: This information is for educational purposes only and should not be considered investment advice. Please do your own research before making any financial decisions.