Published on May 4, 2025 | 📊 Stock Analysis | 🛒 Avenue Supermarts Ltd (DMart)

🏢 Company Overview: Avenue Supermarts Ltd (DMart)

Avenue Supermarts Ltd (NSE: DMART, BSE: 540376) operates India’s most trusted value retail chain, DMart, founded by legendary investor Radhakishan Damani. Known for its cost-efficient, customer-first retail model, DMart has consistently expanded in Tier-1 to Tier-3 cities, offering grocery, home essentials, and general merchandise at competitive prices.

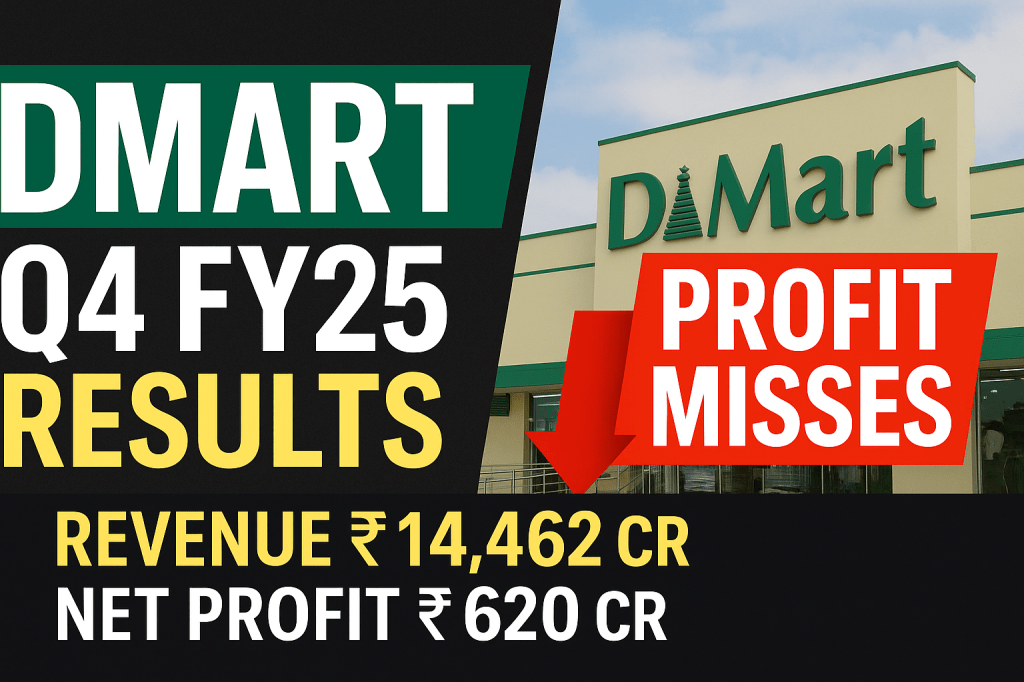

📊 Q4 FY25 Financial Results – Quick Snapshot

| Metric | Q4 FY25 (₹ Cr) | Q4 FY24 (₹ Cr) | YoY Growth |

|---|---|---|---|

| Revenue from Operations | ₹14,462.39 | ₹12,393.46 | 🔼 16.7% |

| Net Profit | ₹619.71 | ₹604.20 | 🔼 2.6% |

| EPS (Basic) | ₹9.52 | ₹9.28 | 🔼 |

| EBITDA Margin (approx.) | ~9.8% | ~10.3% | 🔽 |

📉 Quarter-over-Quarter (QoQ): Revenue down 7.1%, and net profit fell 21% sequentially due to softer demand and margin pressures.

🔁 Full-Year Performance: FY25 vs FY24

| Metric | FY25 (₹ Cr) | FY24 (₹ Cr) | Growth |

|---|---|---|---|

| Total Revenue | ₹57,789.81 | ₹49,532.95 | 🔼 16.7% |

| Net Profit | ₹2,927.18 | ₹2,694.92 | 🔼 8.6% |

| EPS | ₹44.98 | ₹41.43 | 🔼 |

| Total Assets | ₹24,891.47 | ₹21,566.12 | 🔼 15.4% |

🧠 Takeaway: Strong full-year revenue and profit growth. However, Q4 numbers suggest near-term headwinds.

📈 Shareholding Pattern – March 2025

| Category | Holding (%) | Change from Dec 2024 |

|---|---|---|

| Promoters | 74.66% | ➖ No Change |

| Foreign Investors | 8.11% | 🔼 +0.5% |

| Domestic Institutions | 7.03% | 🔽 -0.25% |

✅ Positive: FII increasing stake indicates global investor confidence

❌ Slight Concern: DII booking minor profits

🔍 Key Financial Ratios (FY25)

- 📌 Current Market Price (CMP): ₹4,200

- 💼 Market Capitalization: ₹2,73,200 Cr

- 📊 P/E Ratio: 93.4x (very high)

- 💰 ROE: 13.6%

- 🏦 ROCE: 16.2%

- ⚖️ Debt-to-Equity Ratio: 0.03 (excellent)

🚀 DMart’s Strategic Plans & Future Outlook

📦 Expansion Focus:

- Aggressive store openings in smaller cities

- Expanding DMart Ready for online grocery delivery

⚙️ Operational Enhancements:

- Automation in logistics and warehousing

- Better sourcing to improve margins

💡 Challenges Ahead:

- High inflation affecting discretionary demand

- E-commerce competition from Amazon, Flipkart, JioMart

🧠 Expert ChatGPT Verdict: Invest, Hold, or Avoid?

✅ Why You Should Consider Investing:

- 📈 Consistent growth with proven retail model

- 🔄 Low debt with high return ratios

- 🌍 Increasing foreign investor interest

- 🛒 Consumption play with long-term growth potential

❌ Risks to Watch:

- ⚠️ High valuations (P/E > 90)

- 📉 Q4 weakness in profitability

- 🧾 Competitive pressure from e-commerce and modern trade

🔍 Final Recommendation: Hold / Accumulate on Dips

DMart remains a long-term compounder, but the current valuation suggests limited short-term upside. Investors should consider accumulating on corrections below ₹3,900–₹4,000.

📢Disclaimer: This information is for educational purposes only and should not be considered investment advice. Please do your own research before making any financial decisions

Enjoyed this post? Like, Comment & Follow my blog for more insightful content!