📅 Updated: April 2025

🏢 Company Overview: Adani Energy Solutions Ltd (AESL)

Earlier known as Adani Transmission Ltd, AESL is a prominent name in India’s energy transmission, power distribution, and smart metering segments. The company operates across 14 Indian states and is a crucial enabler in the nation’s transition to a greener, smarter power infrastructure.

🔍 Q4 FY25 Performance Snapshot (YoY)

| Metric | Q4 FY25 | YoY Growth |

|---|---|---|

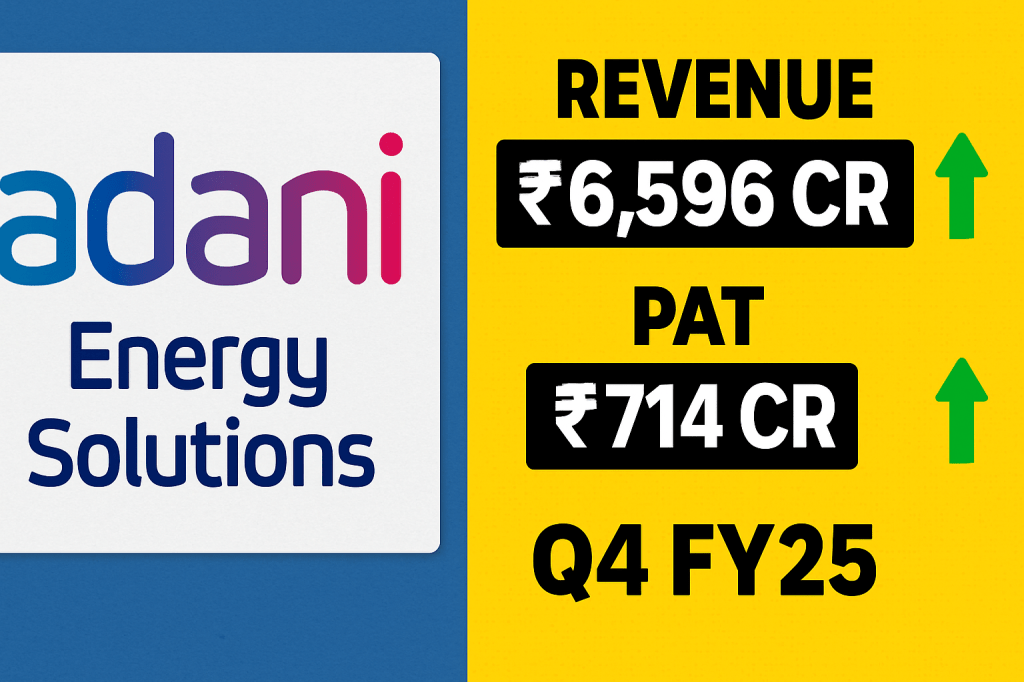

| 💰 Revenue | ₹6,596 Cr | ▲ 36% |

| ⚙️ EBITDA | ₹2,262 Cr | ▲ 28% |

| 🧾 Net Profit | ₹714 Cr | ▲ 87% |

📈 FY25 Full-Year Performance

| Metric | FY25 | YoY Growth |

|---|---|---|

| 💸 Revenue | ₹24,447 Cr | ▲ 42% |

| 📊 EBITDA | ₹7,746 Cr | ▲ 23% |

| 📈 Net Profit | ₹2,427 Cr | ▲ 103% |

| 🏗️ Capital Spend | ₹11,444 Cr | ▲ 104% |

| 💼 Net Borrowing | ₹30,076 Cr | — |

| 📉 Debt/EBITDA | 3.2x | Improved |

✔️ Strong revenue and earnings growth driven by new project commissions, enhanced smart meter deployment, and increased energy sales in key regions.

🔌 Business Breakdown

🛰️ Transmission

- 🔧 Network length: 26,696 circuit km

- 🔌 Capacity: 90,236 MVA

- ✅ Added 7 new projects this year

- 📊 Availability: ~99.7%, highlighting operational efficiency

🏙️ Power Distribution

- 🔋 Units Delivered: 10,558 MUs (+6% YoY)

- ⚡ Losses Reduced: 4.77% vs 5.29% last year

- 🌿 Renewable Contribution: 36%, with a goal of 60% by FY27

📡 Smart Metering

- 🔄 Installed: Over 3.1 million meters

- 🎯 Target: 10 million by FY26

- 📦 Awarded Orders: Covering 22.8 million meters (₹272 bn value)

📌 Key Financial Metrics

- Current Market Price (CMP): ₹1,050 (approx.)

- Market Capitalization: ₹1.2 lakh crore+

- P/E Ratio: ~50x

- Return on Equity (ROE): ~15%

- Return on Capital (ROCE): ~9%

- Debt-to-Equity: ~2.6x

👥 Shareholding Structure

- 🧑💼 Promoters: Hold ~69.9% stake (Adani Group)

- 🌐 Institutional Stakeholders: Qatar Investment Authority owns 25.1% in its Mumbai electricity business (AEML)

- 💼 Strong institutional trust reflects confidence in AESL’s business model

🌱 Sustainability & ESG Progress

AESL has made substantial progress in its sustainability agenda:

- ✅ Zero-Waste and Single-Use Plastic-Free certified

- ✅ Water Positive Status across multiple locations

- ✅ GHG Emissions reduced by 53% from FY19 levels

- ✅ ESG Ratings:

- MSCI: BB

- S&P Global: 73/100

- FTSE: 4.4/5

♻️ The company aims to source 60% of its energy from renewables by FY27.

✅ Investment Merits

🔹 Consistent Financial Upside

🔹 Massive Infrastructure Pipeline

🔹 Rapidly Growing Smart Meter Footprint

🔹 Stable & Predictable Revenues (via regulatory tariff model)

🔹 Positive ESG Credentials & Institutional Trust

⚠️ Key Risks

🔸 Leverage Level: Though improving, debt remains relatively high

🔸 Operational Execution: Scaling up metering and infra projects comes with risk

🔸 Premium Valuation: Current P/E suggests expectations of continued high growth

📊 Analyst Takeaway

AESL is rapidly evolving into a full-spectrum utility provider, well-placed to support India’s goal of 500 GW clean energy capacity by 2030. Its smart metering contracts, expanding transmission network, and ESG-aligned business model make it a solid long-term play.

🔎 Investment Outlook:

✅ Suitable for long-term ESG and infrastructure-focused portfolios

📝 Conclusion

AESL is much more than a traditional utility—it’s a futuristic platform powering India’s clean and connected energy vision. With a forward-looking strategy and strong fundamentals, it remains one of the most promising picks in the energy infrastructure segment.

📢 Stay Connected!

For more earnings insights, green investment ideas, and utility sector updates — keep following our blog!