Indian Renewable Energy Development Agency Ltd. (IREDA) has become one of the most talked-about PSU stocks after its impressive listing and stellar Q4 FY25 performance. Let’s break down why this government-backed green energy financier is catching investor attention.

🔍 Company Overview

IREDA is a government-owned NBFC that focuses on financing renewable energy projects in India. With India pushing for 500 GW of green capacity by 2030, IREDA stands at the forefront of this energy transition.

🧾 Key Q4 FY25 Highlights

- Revenue: ₹6,745.78 Cr 🚀

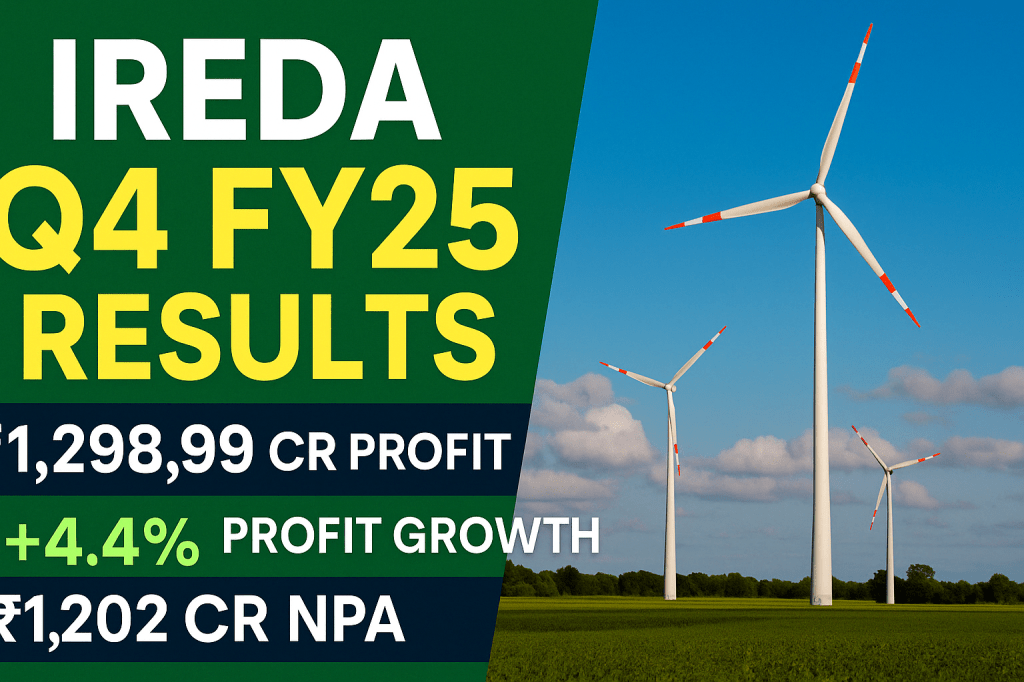

- Net Profit: ₹1,298.99 Cr 💰

- Sales Growth (YoY): 37.9% 📊

- Profit Growth (YoY): 44.4% 📈

- Return on Equity (ROE): 10.89%

- ROCE: 10.47%

- Debt-to-Equity: 5.01

- Price to Earnings (P/E): 10.71

- Market Cap: ₹4,361 Cr

- CMP: ₹181.40

💼 Promoters & Institutional Confidence

✔️ 75% stake held by the Government of India

✔️ Increasing public and mutual fund interest

✔️ Backed by institutions like LIC, SBI MF, and global development banks

✅ Why You Might Consider Investing in IREDA

🌿 Green Energy Momentum – Financing India’s clean energy revolution

🏢 Strong Fundamentals – ROE and Profit growth are solid

💸 Low Valuation – A P/E of 10.71 for a growing NBFC is attractive

🏦 Diversified Borrowing – Borrowing from EIB, JICA, SBI, etc. ensures funding stability

🟢 High Impact Sector – Aligned with India’s ESG and climate goals

⚠️ Risks & Concerns

📉 High Leverage – Debt to Equity ratio at 5.01 is a watchpoint

📊 Rate Sensitivity – Rising interest rates can impact margins

⚖️ Legal Gray Zone – ₹1,200 Cr under NPA classification dispute

🏛️ Policy-Driven – Government interference risk for PSUs

🔮 Outlook: What Lies Ahead?

With a solid loan book, reduced cost of borrowing, and a central role in India’s renewable mission, IREDA is poised for long-term growth. Analysts believe that continued earnings visibility and expanding margins could lead to a re-rating in FY26.

🧠 Expert View:

IREDA offers a rare blend of government backing, clean energy exposure, and undervalued pricing. It’s one of those green economy plays where patience might pay off big.

💡 Verdict: Buy on Dips – Long-Term Play for ESG-focused investors

📌 Disclaimer: This blog is for educational purposes only and not investment advice. Please consult a financial advisor before investing.

Enjoyed this post? Like, Comment & Follow my blog for more insightful content!